Tax Law Services in New York

Tax Law Services in New York

IRS Problems, State Tax Disputes, and Tax Planning — Handled by an Attorney with an LL.M. in Taxation and admitted to the U.S. Tax Court.

Last reviewed by Attorney Ronald S. Cook — May 2026

Tax problems do not resolve themselves — they compound. Unfiled returns generate penalties and interest. Ignored IRS notices escalate to liens, levies, and wage garnishments. Unresolved state tax debts lead to license suspensions, bank freezes, and asset seizures. The longer you wait, the fewer options you have and the more it costs to fix.

Attorney Ronald S. Cook holds an LL.M. in Taxation in addition to his J.D. and MBA — a level of specialized tax training that most attorneys and most CPAs do not have. That distinction matters when you are negotiating with the IRS, contesting a state tax assessment, or structuring a transaction to minimize tax exposure.

Call (888) 275-2620 or text (631) 678-8993 for a free consultation. Available 24/7.

IRS Disputes and Federal Tax Matters

Audits and Examinations

If you have received an IRS audit notice (Letter 2202 or similar), you have the right to representation. An audit does not mean you owe money — it means the IRS wants to verify information on your return. The outcome depends on how the audit is handled: what documentation is provided, what positions are taken, and how the case is presented to the examining agent. Attorney representation during an audit is protected by attorney-client privilege — a protection that CPAs and enrolled agents cannot offer to the same extent.

Offers in Compromise (OIC)

An Offer in Compromise allows you to settle your federal tax debt for less than the full amount owed. The IRS evaluates OIC applications based on your ability to pay, income, expenses, and asset equity using a formula set out in the Internal Revenue Manual (IRM 5.8). Not everyone qualifies — and submitting an OIC that the IRS will reject wastes time and money. Proper financial analysis before filing is critical.

Installment Agreements

If you cannot pay your tax debt in full, the IRS offers several installment agreement options under IRC § 6159 — including streamlined agreements (for debts under $50,000), partial-pay installment agreements, and non-streamlined agreements requiring full financial disclosure. The right structure depends on the amount owed, your income, and your assets.

Tax Liens and Levies

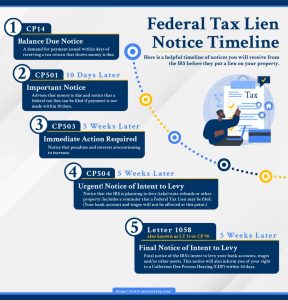

A federal tax lien (IRC § 6321) attaches to all of your property — real estate, vehicles, bank accounts, accounts receivable — the moment an assessment is made and you fail to pay after demand. A levy (IRC § 6331) is the actual seizure of property to satisfy the debt. Bank levies freeze your accounts. Wage levies garnish your paycheck. If you have received a Notice of Federal Tax Lien (NFTL) or a Final Notice of Intent to Levy (Letter 1058 / LT11), you have rights — including the right to a Collection Due Process (CDP) hearing under IRC § 6330 — but the deadlines are strict.

Unfiled Returns

If you have one or more years of unfiled federal tax returns, the IRS can file a Substitute for Return (SFR) on your behalf — and SFRs are calculated without any deductions, credits, or exemptions you would have claimed. The result is almost always a tax bill far larger than what you actually owe. Filing delinquent returns with proper preparation often dramatically reduces the assessed liability and is typically the first step toward resolving the situation.

Penalty Abatement

The IRS imposes penalties for late filing (IRC § 6651(a)(1)), late payment (IRC § 6651(a)(2)), and accuracy-related issues (IRC § 6662). These penalties add up fast — the late filing penalty alone is 5% per month up to 25% of the unpaid tax. However, the IRS can abate penalties for reasonable cause (IRM 20.1.1.3) or under the first-time penalty abatement (FTA) waiver if you have a clean compliance history for the prior three years.

Innocent Spouse Relief

If your spouse or former spouse understated income or claimed improper deductions on a joint return, you may be eligible for Innocent Spouse Relief under IRC § 6015, which can relieve you of liability for the tax, interest, and penalties attributable to the other spouse’s errors. There are three forms of relief — innocent spouse (§ 6015(b)), separation of liability (§ 6015(c)), and equitable relief (§ 6015(f)) — each with different requirements and deadlines.

New York State and Local Tax Matters

New York State Income Tax

The New York State Department of Taxation and Finance conducts its own audits and assessments independent of the IRS. If you are audited by the state, you have the right to challenge the assessment through the Bureau of Conciliation and Mediation Services (BCMS) and, if unresolved, through the Division of Tax Appeals (DTA). State tax penalties and interest accrue separately from federal.

Sales Tax Issues

New York sales tax compliance is a significant issue for businesses. The Department of Taxation and Finance aggressively audits businesses for uncollected or unremitted sales tax. Sales tax assessments can include personal liability for responsible persons under Tax Law § 1133. Sales tax debt is not dischargeable in bankruptcy — making resolution outside of bankruptcy essential.

Property Tax Grievances

If your property is overassessed, you have the right to file a grievance with your local Board of Assessment Review (RPTL § 524) and, if denied, a Small Claims Assessment Review (SCAR) petition or an Article 7 proceeding in Supreme Court (RPTL § 700 et seq.). Deadlines are strict — Grievance Day is typically the third Tuesday in May for most Nassau and Suffolk County municipalities. Successful grievances reduce your assessed value and your tax bill going forward.

Warrants and Collection

New York State can file a tax warrant — the equivalent of a judgment — without going to court (Tax Law § 692(c) for income tax, § 1138(a) for sales tax). A warrant allows the state to levy bank accounts, garnish wages, seize assets, and place liens on real property. If you have received a warrant or a Notice of Proposed Assessment, act immediately.

Tax Planning and Transactional Tax

Business Formation and Structure

The choice of entity — sole proprietorship, LLC, S-Corp, C-Corp, partnership — has direct tax consequences for income allocation, self-employment tax, payroll tax, and eventual sale or dissolution. Proper structuring at formation avoids costly restructuring later. Attorney Cook’s combined tax LL.M. and MBA background is directly applicable to entity selection, operating agreement drafting, and tax-efficient business planning.

Estate and Gift Tax Planning

New York imposes its own estate tax (Tax Law Article 26) with an exemption threshold significantly lower than the federal exemption. As of 2025, the New York estate tax exemption is approximately $6.94 million — and New York’s “cliff” provision means that estates exceeding the exemption by more than 5% lose the exemption entirely and are taxed on the full value. Coordinated federal and state estate tax planning — including the use of revocable trusts, irrevocable trusts, Medicaid Asset Protection Trusts, gifting strategies, and life insurance planning — is essential for New York residents with significant assets.

Real Estate Tax Issues

IRC § 1031 like-kind exchanges, installment sales (IRC § 453), capital gains planning, New York State transfer tax (Tax Law § 1402), New York City Real Property Transfer Tax, and mansion tax considerations. Real estate transactions in New York carry multiple layers of tax exposure — federal, state, and local — that must be analyzed before closing.

Tax and Bankruptcy

Certain tax debts can be discharged in Chapter 7 bankruptcy — but only if they meet specific criteria under 11 U.S.C. § 523(a)(1) and the applicable timing rules (the “3-year rule,” “2-year rule,” and “240-day rule”). Other tax debts — including trust fund taxes, fraud penalties, and unfiled return assessments — are generally non-dischargeable. Attorney Cook’s dual LL.M. degrees in both Taxation and Bankruptcy provide an uncommon combination of expertise for clients whose tax problems and debt problems intersect.

Why Clients Choose Ronald S. Cook, P.C.

- LL.M. in Taxation — graduate-level tax law training beyond the J.D.

- LL.M. in Bankruptcy — critical for clients whose tax and debt issues overlap.

- MBA — financial and business analysis that informs every tax strategy.

- Prior Wall Street experience — a background in finance that most tax attorneys lack.

- Thousands of five-star reviews from clients across New York.

- Available 24/7.

- Suffolk and Nassau County offices — Smithtown and Garden City.

View all books by Attorney Cook on Amazon.

Free Consultation — Call Now

If you are dealing with an IRS audit, a tax lien or levy, unfiled returns, a state tax assessment, or need tax planning advice, contact us today. We will review your situation and tell you where you stand.

Call (888) 275-2620 · Available 24/7

Free consultation · All 62 New York counties – Fedral Tax issues handled nationwide.

Related: Bankruptcy & Debt · Estate Planning · Business Law · Civil Litigation · Real Estate

Last reviewed by Attorney Ronald S. Cook — April 2026

This page is for informational purposes only and does not constitute legal advice.